Value of domestic deals has tripled, outbound deals up 275 per cent, as inbound deals see decline

Even as the global COVID-19 pandemic threatens to enter a fourth wave in North America despite the steady rollout of a vaccination program, corporate Canada is looking at some of the strongest dealmaking in years, says a new report by Torys LLP.

"It has been incredibly busy," says Torys' partner John Emanoilidis, noting that domestic deal volume increased 49 per cent in the first half of 2021, compared to the same period last year. As well, Canadian dealmakers are also broadening their reach to access larger markets in the U.S. and around the world, with the total value of Canadian outbound M&A already surpassing 2020 levels.

"The drive to do strategic deals has returned, and we're seeing Canadian companies making some bold plays that reflects their high level of confidence," says Emanoilidis, adding that these deals are aided by low debt financing costs. Private equity also continues to make its presence known on the M&A scene, with a lot of "dry powder" cash on hand.

Emanoilidis, who co-heads Torys' M&A practice with partner Michael Amm, says that with signs of economic recovery encouraged by COVID-19 vaccination programs, all indications are that strong equity markets and an abundance of capital will help maintain dealmaking momentum through this year and beyond. That is even despite the recent surge in cases among the unvaccinated.

Amm agrees, saying, "it really is quite something – we are seeing incredible activity in deal volume and deal size." Clients on the acquisition side have spent the pandemic focused on understanding the key strategic objectives of their business, Amm says, and are now ready to execute on important deals that will move them ahead.

Looking at domestic M&A, the Torys report points out that aggregate deal value has tripled, thanks to some large transactions. There were 918 deals in the first half of 2021, compared to 615 in the first half of 2020, the report says, while the deal value so far this year totaled $87.9 billion, compared to $14.12 billion the same period a year earlier.

One example includes a deal under which Rogers Communications Inc. would acquire all Shaw Communications Inc.'s issued and outstanding Class A shares and Class B shares. It's a transaction valued at approximately $26 billion, one of the largest domestic M&A deals in the last decade.

The elevated equity prices for publicly traded companies are also providing strategic buyers with "strong acquisition currency," Emanoilidis says, noting a larger proportion of deals now involve share consideration, either with additional cash or without.

As for "outbound" M &A, the Torys report says the United States remains the destination of choice for Canadian strategic and financial buyers. Macro-economic factors are significant drivers of heightened cross-border deal activity, the report says, with access to larger markets, expansive continental reach and the low cost of debt remaining important for dealmakers. To the end of June, there were 715 deals worth about $100 billion, compared to 996 deals worth $81 billion in all of 2020.

As one example, the report cites the recently proposed merger of railways CN and Kansas City Southern, a deal worth US$33.6 billion to create a North American railway connecting ports and rails across the United States, Mexico and Canada.

Beyond the U.S., Canadian dealmakers have also been seeking growth opportunities in Europe, with France, the U.K. and Spain appearing in the top five countries with the most capital invested by Canadian investors in 2021 to date. One example is Intact Financial Corporation, together with Tryg A/S, recently completing a £7.2 billion acquisition of RSA Insurance Group plc.

Credits: Bloomberg, Torys

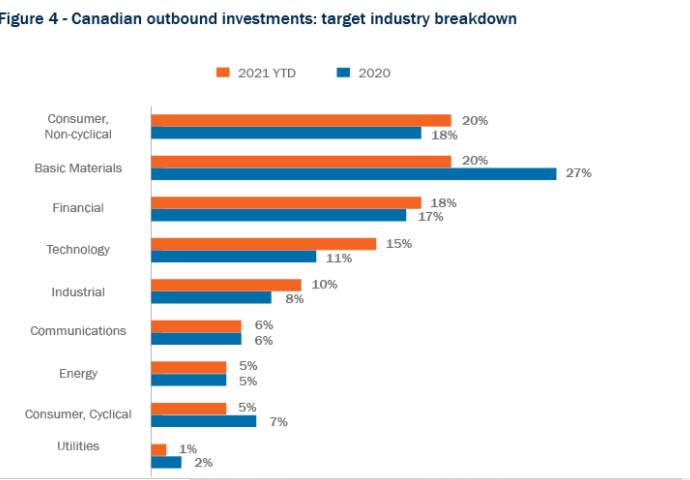

The Torys report says the technology sector has had the most vigorous growth among sectors in Canadian outbound investments, with a four-percentage point increase in total deal value recorded so far this year relative to 2020.

Technology has shown resilience to the effects of the pandemic, the report adds. As the pandemic forces people and businesses to carry on business remotely, companies reassessed, and in many cases, expanded or evolved their technology use and digital strategies to maintain competitive strength and increase revenue growth.

"The expansion of online commerce, video and electronic communications technology and innovative healthcare research and applications are some recent examples of technology industries in transformation."

Amm says he is generally surprised by the "broad nature" of the sectors that have seen meaningful deal activity. Some sectors are "consistently" hot, he says, except for perhaps the energy sector. "There are obviously deals being done," he says, but given the economic slowdown, and the focus on green credentials, dealmaking has been a bit more tepid.

Emanoilidis say this surge in outbound activity is a recognition by corporate Canada of the need to build scale and accelerate growth in international markets as the world is seen to be emerging – slowly – out of the pandemic. "There is recognition that it is important to have global scale."

He adds that private equity and pension funds, looking for good returns on the cash they are sitting on, have been active in outbound deal activity, especially with infrastructure and real estate aspects.

While outbound and domestic dealmaking has grown, the Torys report notes that, on an annualized basis, the aggregate value of foreign investment in Canada appears to be on the decline relative to deal activity recorded in 2020, with total deal value projected to be approximately $44 billion in 2021 (based on the $22 billion worth of deals in the first half), compared to $53 billion in 2020.

However, activity levels are strong and should surpass the peak level recorded in 2019, the report says. The U.S. remains the largest inbound source of foreign investment in Canada. A good example is Goldman Sachs' $1.3 purchase of Winnipeg-based group benefits provider People Corporation.

While most deals – about 60 per cent - were valued at less than $100 million, the report notes there has been a three per cent increase in deals valued between $500 million and $1 billion.

"Canada is still seen as a desirable destination for investment," says Emanoilidis, noting the country's skilled workforce and stable political environment.

Amm says the impact of travel restrictions has also been part of the relatively slower pace of inbound deals, as well as more of a focus on home countries and "what I'd call domestic resiliency." The Canadian government, for example, has telegraphed that it will be scrutinizing proposed acquisitions by foreign entities to make sure they won't compromise national interests. There have also been fewer deals involving China, thanks to some political tensions between the two countries and the increased regulatory hurdles.

"We're seeing governments increasingly vigilant on the regulatory front," Amm says, whether it is with regulated industries or general industries where there is a competition concern.

Lawyers working with clients on M&A have adapted well to the "new norm" of the pandemic, with less personal interaction and fewer site visits and more zoom calls. "Technology has certainly helped bridge the gap, especially on cross-border deals and the restrictions on travelling," says Emanoilidis. Some of the use of virtual technology will likely continue post-pandemic, given the efficiency, "but not in all cases – there is a real desire for people to see each other."

Looking to the future, both Amm and Emanoilidis say they expect deal activity to increase and that while valuations are relatively high, it hasn't reached the level of "irrational" exuberance. Says Amm: "We are still at the stage of highly strategic and quite disciplined transactions, which include significant deals that I would call bold.

"There's a lot of appetite out there i- buyers have cash and financing capability, while sellers are seeing the higher valuations." In the longer term, the potential of higher interest rates and inflation and how much taxes will have to rise to pay the cost of dealing with COVID-19 might influence the level of deal activity.

"But that's not tomorrow, that's further down the line."