Geopolitical, inflation and economic risks keeping more investors on sidelines

Merger and acquisition activity has slowed in the first nine months of this year thanks to economic and geopolitical risk. However, there’s still a lot of interest in dealmaking, with the latest numbers beating those from before the pandemic, say lawyers at Bennett Jones LLP.

“Deals are being done and opportunities are there, but investors are showing restraint and gone are the days of doing a deal at any cost,” says a blog post written by partners Linda Misetich Dann, Christian Gauthier and Harinder Basra.

“When we were talking about writing this piece, we decided that it wasn’t really useful making a lot of comparisons of this year to 2021 or 2020, for obvious reasons, the pandemic,” Gauthier says.

“2020 saw a lot of M&A activity stop because of COVID-19, and 2021 was super, super busy as making deals took off like never before. So, comparing current figures to those before the pandemic makes more sense.”

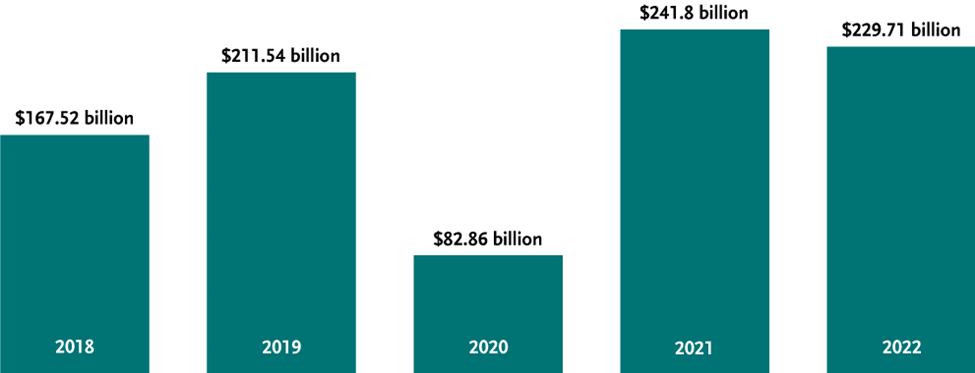

Looking at M&A volume for the first three quarters of the past five years shows that investors are willing to make deals. While the first three quarters of 2022 saw deal volume drop compared to a recording-breaking number for the same period in 2021, that volume is still higher than the first three quarters of 2019, the last full year not affected by the pandemic.

M&A volume in the first nine months of 2022 was US $229.7 billion, down from US $241.8 billion for the same period in 2021 but higher than the US $211.54 billion recorded in 2019. The first nine months also saw a higher volume of deals than the full-year volume of US $225.7 billion in 2018.

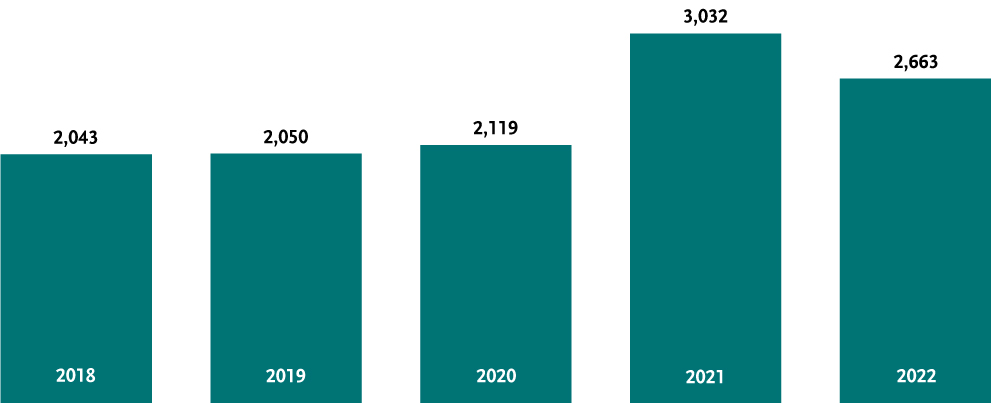

As for the number of deals, there were 2,663 in the first three quarters, about 30 percent higher than in 2019 (2,043) and 2018 (2,050). The deals so far this year are only slightly short for all of 2019 (2,753) deals in 2019 and 2018 (2,804).

Gauthier says that while the value of deals in a particular period is an important factor in assessing M&A activity, the number of deals is “often a better gauge of appetite in dealmaking, as one megadeal can affect the total value.”

Still, the blog post notes the significant challenges for M&A moving into the final three months of 2022. “Central banks around the world continue to increase interest rates in their fight against inflation and have signalled that rates will continue to rise in the near term.” The lawyers also point to concerns about a recession and geopolitical risks such as Russia’s invasion of Ukraine.

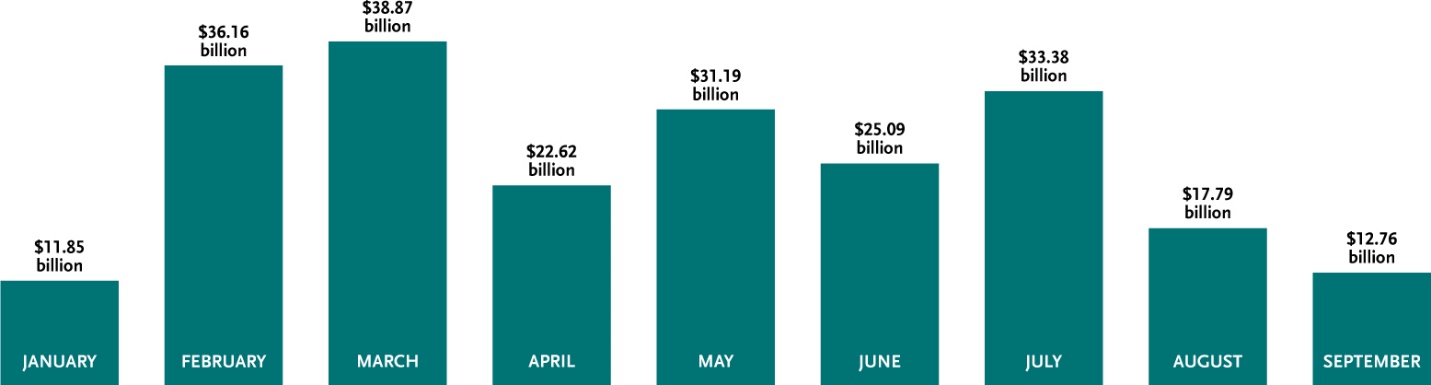

Gauthier says deal volume was down in the third quarter of 2022 to US $63.9 billion from US $78.9 billion in Q2 and US $86.9 billion in Q1. July was a busy month at $33.4 billion in deal volume, but it dropped to US $17.8 billion in August and US $1 2.8 billion, the second lowest monthly total of the year. (The lowest volume was in January, at US $11.85 billion)

“The decline in Q3 deal activity should not be seen as a surprise, though. It is consistent with what the markets have been seeing in the past quarter.”

Gauthier also mentions that more people were taking “well-deserved” time off this summer. “For many, it was the first time they had a vacation in more than two years,” and many organizations told their people to make the most of the opportunity to recharge, Gauthier says. Hence, “the slower M&A deal activity during the past summer is partly a reflection of this.”

Gauthier acknowledges that the activity in the capital markets is “a different story,” with a significant falloff in recent months. “There’s more a herd mentality in the capital markets, so the impact of risk, inflation and other factors is being felt more strongly than M&A,” he says. “With M&A, a lot of sophisticated investors, especially private equity, are playing the long game.”

M&A also typically involves “bigger-ticket” items, with fewer participants, “so there is less of a herd mentality.”

At the same time, M&A activity has likely recently slipped as buyers look at their cost of capital and debt and try to plan for the long term. “They are waiting to see a more stable market “so they can price deals more accurately,” he says. “Sellers are in the process of having to adjust expectations on what they can get for their business. It can take a while for that to happen.”

In such an environment where the gap between buyer and seller expectations can be wide, Gauthier says the role of a lawyer is helping the two parties conclude a deal while finding ways of dealing with potential risk. Earnouts, for example, where a seller can receive more money on a deal post-closing if specific financial metrics are met, is just one tool that lawyers can help structure to help buyers and sellers deal with risk and “have it assigned fairly.”

The demand for base metals, precious metals, and battery metals in the mining sector has increased investor interest in M&A. A July 2022 report by the International Energy Agency said the world needs up to 50 more lithium mines, 60 more nickel mines and 17 more cobalt mines by 2030 to meet the projected demand in electric vehicle battery supply chains.

Lithium has the largest projected demand-supply gap, and nickel is facing a significant demand increase by 2030. “Timing is a serious factor—it takes a minimum of 10 years to bring a mine into production,” even if everything goes right.

The blog says the oil and gas sector “continues to feel the pull” of opposing forces, with tight supply on the one hand and fears of a global recession on the other. “All with the backdrop of the geopolitical uncertainty caused by Russia’s invasion of Ukraine.”

M&A activity in this sector was muted in Q3 thanks to uncertainty and fluctuating oil prices. For example, WTI crude was US $108.43 per barrel at the beginning of Q3 2022 and US $79.49 per barrel by the end of the quarter. That’s a decline of more than 25 percent. However, recently announced oil production cuts have seen prices rise again.

While companies and investors are “forging ahead through choppy seas,” deals are being made, and companies continue to look at potential transactions, depending on market fluctuations that affect decisions. Private equity, in particular, is looking for an opportunity to deploy its cash reserves.

“What’s needed is stability, so buyers and sellers can have a better sense of pricing, execution and risk,” Gauthier says. Stability allows new baselines for post-pandemic performance for companies and their industries. When this happens, “deal activity can be expected to pick up, perhaps quickly.”

Q3 2022 M&A Deal Volume

(Announced, completed or pending deals, excluding those that have been terminated or withdrawn)

Source: Bennett Jones based on Bloomberg data as of September 30, 2022, in US dollars

Deal Count, Q1-Q3 from 2018 to 2022

Source: Bennett Jones based on Bloomberg data as of September 30, 2022, in US dollars

Monthly deal values January-September 2022

Source: Bennett Jones based on Bloomberg data as of September 30, 2022, in US dollars