The proposed deal between Rogers and Shaw is shining a new light on the regulator

It’s not a surprise that, within a few days of Rogers Communication’s announcement on March 15 that it had an agreement to acquire rival Shaw Communications in a blockbuster deal worth $26 billion, Canadians would notice.

Indeed, not long after that announcement, the Competition Bureau Canada, which investigates whether such megadeals could decrease competition in the industry, said it received an unprecedented amount of online feedback. The transaction would combine Canada’s two largest cable operations, which are also rivals in the wireless sector.

If nothing else, we are passionate about cable and wireless services, especially anything that could raise the prices for these services.

“The Competition Bureau is receiving a higher-than-normal number of online questions and feedback following the announcement of Rogers’ proposed acquisition off Shaw,” the regulator said in an online post. It added that the bureau “will review the proposed transaction” and encourages the public to share its views online, as it cannot take phone calls because of the COVID-19 pandemic.

As the business world in Canada and abroad turns to megadeals and consolidation to increase profits and become more efficient, these transactions also have the potential to transform key industries. But there is also concern about whether this will erode competition and, as a result, force consumers to pay more for services. The result is that, these days, Canada’s competition bureau is getting noticed.

With an annual budget of just less than $52 million — a figure that has dropped in real and absolute terms over the last few years — lawyers who specialize in competition law acknowledge that the competition bureau has its work cut out in investigating a growing number of more complex transactions. Some of these deals are in disruptive digital sectors that often involve more than one regulatory body, such as the Canadian Radio-television and Telecommunications Commission. Others also wonder if it is time to look at laws and regulations governing the bureau to see if there can be improvements in some key areas.

Neil Campbell, a partner in the international trade, competition, antitrust and foreign investment practice at McMillan LLP, says the bureau is “an under-resourced agency” given the work it does not only on mergers but other anti-competitive practices, such as price fixing. In today’s economy, “the amount of work has increased, and the funding [of the bureau] has not kept pace,” he says.

“The world is more complex, and a lot more time is needed to effectively deal with the large quantities of electronic documents in complex cases.”

“The economy is transforming,” says Navin Joneja, a partner at Blake Cassels & Graydon LLP, “and I think COVID has really accelerated a lot of the digitization of businesses. And so, you must sometimes view these particular issues through a competition lens; but a lot of times, they also bring up other public policy issues, like privacy and misinformation.”

Campbell’s colleague at McMillan, partner James Musgrove, agrees, noting that the bureau’s budget is now about $2 million lower than it was a decade ago. Staffing at the bureau is also lower, with about 380 people compared to about 440.

“On top of that, the world is complicated when we look at the competition law issues, not just in Canada, but around the world,” says Musgrove, who is a past chairman of the Canadian Bar Association National Competition Law Section. He also notes that the bureau often deals with large companies that have the resources to make their arguments on why a deal is not anti-competitive.

At a time when consumer-oriented proposed mergers — such as the Rogers and Shaw combination — has attracted a lot of attention not only in the media but with Canadians in general, the workload has also increased. The filing fees the bureau charges for a merger review (typically around $75,000) likely don’t make up for the growing workload.

Michael Kilby, a partner and the head of Stikeman Elliott LLP’s competition and foreign investment group, says the complexity of these cases, especially in the digital markets and digital economy, “raise novel issues that require different ways of thinking and different modes of analysis.

“I think it’s fair to say that, over the years, the burden on the bureau, the workload on the bureau has increased.”

As for tools and mechanisms of the bureau, Kilby says there has been a lot of attention paid to at least one part of Canada’s competition laws unique to this country — the so-called “efficiencies” argument. Companies can make this argument to get a deal through the bureau review process even though that merger might decrease competition.

Section 96 of the Competition Act limits the bureau’s ability to intercede if companies show that expected efficiencies from a merger would eclipse any potential reduction of competition. These efficiencies do not necessarily have to flow down to the end consumer in the form of lower prices.

Without weighing in one way or another on the debate, Kilby notes that the efficiencies exception “creates a tension” in the competing interests surrounding a particular merger. “It’s been a feature of Canadian competition law since the 1980s,” Kilby says. He notes that it has been controversial because it can allow a merger to go through that could potentially raise consumer prices. Companies can also cut costs by “creating efficiencies” through facility closures and job losses.

Subrata Bhattacharjee, a partner with Borden Ladner Gervais LLP, says he feels that the comfort level is generally high in the tools the bureau has at its disposal, with perhaps the exception of the efficiencies provision. “The question that is raised is whether it is a trap door to letting a whole bunch of anti-competitive mergers through,” he says, and even the bureau has expressed frustration with the role of the efficiencies exception.

Adds Bhattacharjee: “The reality is that the efficiencies defence has been relevant in only a handful of mergers, though I think there is a legitimate debate to be had as to whether we still need it or not.”

Melanie Aitken, co-chairperson of the competition, antitrust and foreign investment group at Bennett Jones (US) LLP and a former commissioner of the competition bureau (2009-2012), says the regulator has a “coherent” framework and sufficient time frame for reviewing mergers with which to work. This framework includes the significant ability to require parties to respond to extensive information requests before being allowed to close.

She also notes that the bureau is an investigative body that does not turn down prospective mergers — although it can challenge the proposed transaction, which then goes to a competition tribunal. This setup is unlike the European Union antitrust regulatory body, which investigates and rules for or against a proposed merger but can also approve or not approve a merger.

She says official notification of a proposed merger or acquisition in the “notifiable” category triggers a 30-day statutory waiting period where the bureau needs to approve the transaction. For most non-complex mergers or acquisitions, the bureau generally responds within about two weeks.

For those complex transactions or those that raise competition concerns, the bureau can issue an additional information request to get extensive additional information from the merging parties, which triggers a second 30-day waiting period. That period only starts when the bureau receives complete responses from the parties. A proposed transaction cannot close until those commitments and potentially other requirements have been satisfied or waived by the bureau.

Aitken notes that the bureau’s current head, Matthew Boswell, has also talked about studying potential changes to the efficiencies defence. However, Parliament has not proposed a change. So long as the efficiencies defence exists, she disputes the bureau’s current stated policy to look at this defence only after reviewing any anti-competitive impacts against which to trade off any efficiencies. The bureau insists on agreement from the parties for extra time, potentially extending to a couple of months, to review the deal if a party raises the efficiencies defence.

“I understand why [the bureau] feels it has time pressures,” she says. But Aitken adds that she doesn’t agree they have the jurisdiction to tie the merging parties’ ability to use the efficiencies defence to the parties agreeing to more review time, especially when the second request model already provides more time.

Aitken also thinks the competition bureau should “focus more on its enforcement mandate” rather than producing broad market studies on different sectors, especially if there is pressure on financial resources on the regulator. She suggests focused reviews of truly problematic transactions or practices are generally a better way to go.

Campbell and Musgrove at McMillan agree. “Market studies are a kind of an open-ended, nonspecific investigation,” Campbell says. “They run on for years, spend millions and achieve very little. I think they’re better off spending their money on real cases, real facts.”

Aitken adds that if there ever is a time for antitrust regulators to try to secure additional resources, “this is it.”

“Antitrust is sexy these days,” she says, especially when it comes to the question of powerful digital players. Regulators worldwide are focused on these FANGA firms — Facebook, Apple, Netflix, Google and Amazon.

“They are very big in the public’s imagination right now and big with politicians,” Aitken says. To the extent that people will look to the competition agencies to solve some of the issues that come from these firms’ position in the market, a review of the regulators’ resources is better than outlawing through legislation specific types of acquisitions these companies might make.

While competition bureau merger reviews may be a sexy topic these days, Joneja at Blakes offers a reminder about the intense interest in megadeals like the proposed Rogers-Shaw transaction. “It is essential to keep in mind that the vast majority of deals in Canada, even ones that require mandatory review by the bureau, don’t raise competition issues.

“When these deals come up, there’s always some discussion of the need for a review, but for the most part, the bureau is doing what is supposed to do.”

Superior Plus Corp. and Canexus Corp, 2016: The Canadian regulator approved the merger based on the efficiencies defence, but the FTC did not approve it. Superior withdrew its offer to buy Canexus after the two could not agree on a required extension because the FTC had blocked the deal.

Staples and Office Depot, 2016: The two office supply retailers saw their proposed merger challenged by the bureau and the U.S. Federal Trade Commission when announced in 2015. The deal was scrapped by the two parties in 2016 after the FTC said it would harm competition.

Tervita, 2015: The hazardous waste company had bought an additional site, giving it three of the four permits in the Northern B.C. market. The bureau’s commissioner opposed the transaction, and a tribunal ordered a divestiture. The case went to the Supreme Court of Canada, which ruled that all that is required for the efficiencies defence to succeed is that they outweigh the competitive harms.

Superior Propane Inc. and ICG Propane Inc., 2003: Perhaps the most contentious merger the bureau has taken on, Superior had a long-running battle with the regulator over its 1998 purchase of ICG. The case ended up at the Federal Court of Appeal, which denied the bureau’s request to overturn the competition tribunal’s decision to allow the purchase in 2003. Tribunal members concluded that, while the transaction created a monopoly in some areas, resulting efficiencies outweighed the costs of reduced competition. The bureau decided not to take the case to the Supreme Court of Canada.

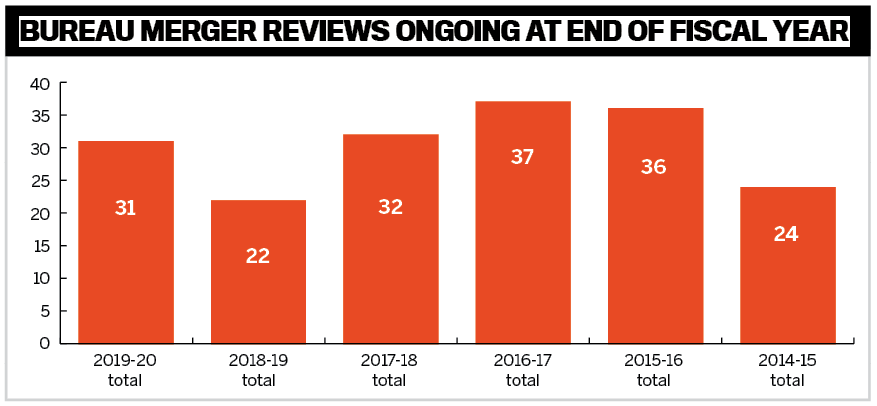

|

2019-20 total |

2018-19 total |

2017-18 total |

2016-17 total |

2015-16 total |

2014-15 total |

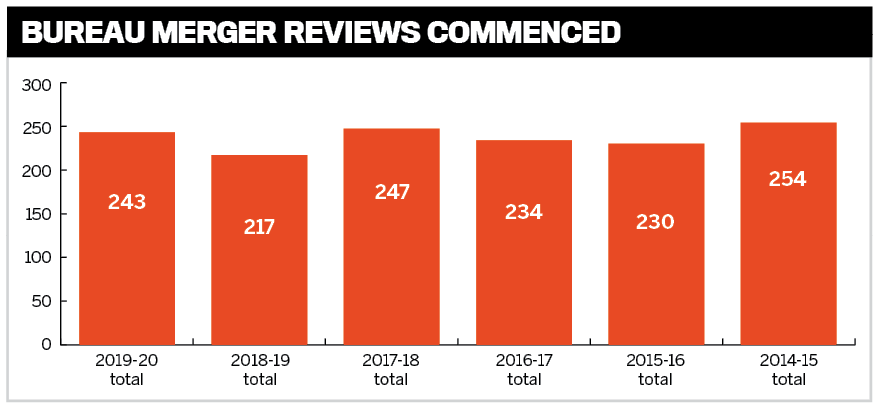

|

243 |

217 |

247 |

234 |

230 |

254 |

|

2019-20 total |

2018-19 total |

2017-18 total |

2016-17 total |

2015-16 total |

2014-15 total |

|

31 |

22 |

32 |

37 |

36 |

24 |